To rationalize my discussion I shall consider thecase: 1.The Impact of Subside on Fuel Price

1. The Impact of Subside On Fuel price: If the government continues to provide subside on fuel price then govt. spending will increase increase in government spending will decrease the National Saving.Because from classical macro economics we know:

National Saving= Total Saving =S= (Y-T-C)+ (T-G)= Private Saving + Public Saving

Here Public Saving = Tax - Govt. Spending

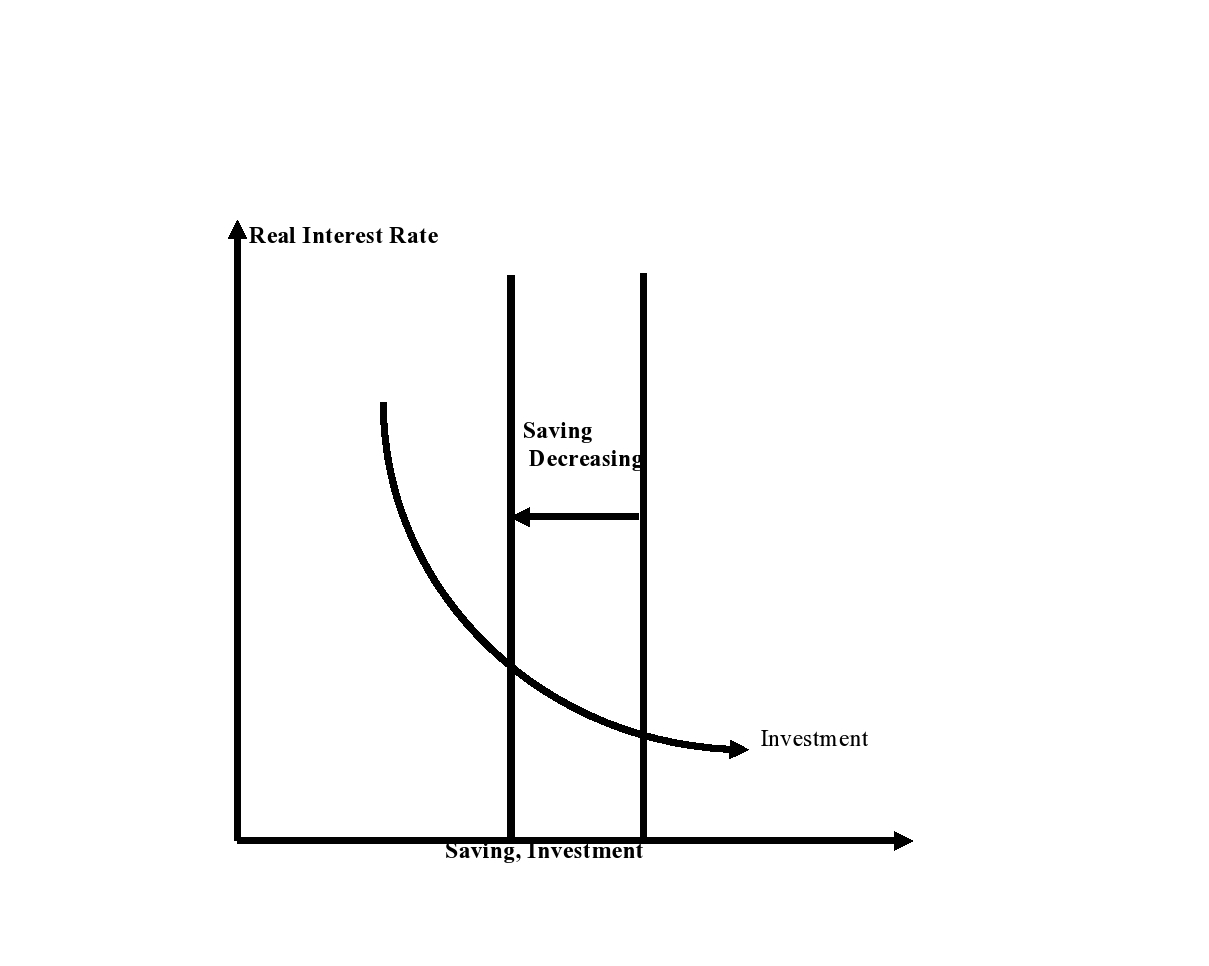

Decrease in national saving will decrease the supply of loanable funds to the Investors. Decrease in supply of loanable funds will increase interest rate. Increase in interest rate will decrease the overall investment in the economy.

Therefore increasing the subside on fuel price will decrease Investment in Private Sector.

The consequences of low investmnets are:

1.Unemployment

2.Availability of low fund to power plant projects

3. Shortage of electricity

4.Low Growth in Industry

5.Low GDP Growth

Therefore to make sure the availability of supply of loanable funds govt. will increase the money supply and inflation will rise. The senior citizens will be harmed by the policy.This will also harm the low income people significantly.

My Opinion regarding the subside of fuel price is quite clear that Govt. should increase the fuel price and subside should not be continued for the long run welfare of Macro Economy.

Executive Summary: Here I have attempted to find out the problems and opportunities of SME in Bangladesh. I clearly acknowledge that I making this paper on the basis of secondary information from Internet and related Jounals published on the topics. The report is not absolutely based on Primary information.

The economy of Bangladesh is at the crossroads. Rapid liberalization has put most existing

industries under severe strain because of their inability to compete with consumer goods being

freely imported after the withdrawal of quantitative restrictions and the drastic reduction of

import tariffs. For the fiscal year 2004-2005, the erstwhile 4-tier duty structure of 7.5, 15, 22.5

and 30 percent has been cut down to 3 tiers, 7.5, 15 and 25 per cent, the weighted average being

16.44 percent. According to the budget speech of the Finance Minister, this would cause an

estimated Bangladesh taka (BDT) 11 billion (USS 186 million) loss of revenue to the

government; but there are no estimates yet about likely losses to the domestic trade and

economy of the country from the flood of imported consumer and industrial products -

cosmetics and toiletries, food and beverages, textiles and apparels, footwear and leather goods,

chemicals and pharmaceuticals, light engineering products, machine tools, hand tools and so on.

All these products (all under the SME category, and the rate at which the glittering

multistoreyed shopping malls are springing up in Dhaka and other major cities of the country is

perhaps a good indicator of the rate of displacement of domestic products by imported

merchandise. Although some producers have been successful in improving their products and significantly increasing external market access, most are languishing.

Both equity and growth being of concern to the Government, the priority is to accelerate

GDP growth in a pro-poor manner from the present 5.5 percent to 8-10 per cent (Annex-I).

Agriculture, besides being the mainstay of the economy, is also important for increasing

employment and reducing poverty. The contribution of agriculture and fisheries to the GDP in

2003-04 was 22.83 per cent at 1995-96 constant prices (crop 12.98 per cent. livestock 2.90

per cent, forestry 1.84 percent, and fisheries 5.15 per cent) (Annex-II) while they provided

over 72 percent of the total employment. Correspondingly, the manufacturing contribution to

GDP in 2003-04 was 16.25 per cent accounting for only 5.4 percent of the total employment.

Whether to achieve the committed Millennium Development Goals (MOGs) of 2015 or the

targets of the National Strategy for Economic Growth, Poverty Reduction and Social

Development, commonly known as the Poverty Reduction Strategy Paper (PRSP), the

development process of Bangladesh must strive to expand employment creation opportunities

very rapidly. The scope of additional absorption of labour in agriculture being somewhat

limited, the best potential for this lies in the manufacturing sector. Inspite of droughts, floods,

cyclones and various other natural or management related disasters, the agricultural sector of

growth of the services sector has also been fairly robust. It is the manufacturing sector's

contribution to the GDP that has remained nearly stagnant at around 15 per cent and its

growth rate at 7.41 percent (estimated values of 2003-04 at 1995-96 constant prices).

NB:from Asia-Pacific Tech Monitor, Sep-Oct 2004 issue, pp. 44-56. Mr. Abdul Awal Mintoo is President of the Federation of Bangladesh Chambers of Commerce and Industry.

Introduction: The abbreviation SME occurs commonly in the European Union and in international organizations, such as the World Bank, the United Nations and the WTO. The term small and medium businesses or SMBs is predominantly used in the USA. EU Member States traditionally have their own definition of what constitutes an SME, for example the traditional definition in Germany had a limit of 255 employees, while, for example, in Belgium it could have been 100. But now the EU has started to standardize the concept. Its current definition categorizes companies with fewer than 10 employees as "micro", those with fewer than 50 employees as "small", and those with fewer than 250 as "medium".By contrast, in the United States, when small business is defined by the number of employees, it often refers to those with fewer than 100 employees, while medium-sized business often refers to those with fewer than 500 employees. Both the US and the EU generally use the same threshold of fewer than 10 employees for small offices (SOHO). In most economies, smaller enterprises are much greater in number. In many sectors, SMEs are also responsible for driving innovation and competition. In India, the Micro and Small Enterprises (MSEs) sector plays a pivotal role in the overall industrial economy of the country. It is estimated that in terms of value, the sector accounts for about 39% of the manufacturing output and around 33% of the total export of the country. Further, in recent years the MSE sector has consistently registered higher growth rate compared to the overall industrial sector. The major advantage of the sector is its employment potential at low capital cost. As per available statistics, this sector employs an estimated 31 million persons spread over 12.8 million enterprises and the labour intensity in the MSE sector is estimated to be almost 4 times higher than the large enterprises. In South Africa the term is SMME for Small, Medium and Micro Enterprises. Elsewhere in Africa, MSME is used for Micro, Small and Medium Enterprises. Industry Canada defines a small business as one that has fewer than 100 employees (if the business is a goods-producing business) or fewer than 50 employees (if the business is a service-based business), and a medium-sized business as fewer than 500. In New Zealand a SME has to be 19 people or fewer.

Abstract: This report is an attempt to find out the financial position of Sonargao Plumbing on the basis of the Financial Statements. We have attempted to find out whether the firm is in a good position or not.After studying the report one will be able find the Answer of the Following questions:

problems of Sonargao Plumbing

Strength & Weakness of Sonargao Plumbing

Growth prospect of Sonargao Plumbing

Introduction: Sonargaon plumbing is a small manufacturer of plumbing supplies located in Sonargoan Narayanganj

In order to answer the Following:

What is the number of shares outstanding? How much Sonargaon Pay in cash Dividends in 2010?

Do any of the ratios Of Soanrgaon Plumbing indicate possible problem areas?

Do the Changes form 2009 from 2010 offer that the firm is growing stronger or weak?

We will calculate the following ratios:

a) Liquidity Ratios: It indicates the extent to which Current Liabilities (CL) covered by assets to be converted to into cash in the near future.

CA

Current Ratio:

CL

CA- Inv.

Quick Ratio:

CL

b) Asset management Ratios: It indicates how well the company is managing its assets.

A/C Receivable

1.Days Sales Outstanding:

Sales /360

Cost of Goods Sold

2.Inventory turnover:

Inv.

Sales

3.Total Asset Turnover:

TA

c) Profitability Ratios: It shows the combined effects of Liquidity, Asset Management and Debt Management on operating results.

Gross Profit

1.Gross Profit Margin :

Sales

EAT

2.Net profit Margin:

Sales

EAT

3.Return On Asset:

TA

EAT

4.Return On Equity:

TE

d) Debt management Ratios:

EBIT

Times Interest Earned(TIE):

I

e) Market value Ratios:

Market Price per Share

1)Price Earning Ratios(PE):

EPS

The Income Statement and Balance sheet for Sonargao Plumbing are given below:

SonargaoPlumbing

Comparative Income Statement

2010

2009

Sales

75,000

70,500

Cost Of Goods Sold

(44,000)

(42,500)

Gross Profit From Sales

31,000

28,000

General And Administrative Expenses

(15,500)

(11,000)

operating Income(EBIT)

15,500

17,000

Interest Expenses(I)

(840)

(10,50)

Pre Tax Income(EBT)

14,660

15,950

Taxes

(4,100)

(44,60)

Net Income(EAT)

10,560

11,490

Dividends Declared And Paid

5,737

4,500

Sonargao Plumbing

Comparative Balance Sheet

2010

2009

Cash

2,280

2,157

Marketable Securities

1,400

1500

A/C Receivables

4,500

2500

Inventories

11,000

6,000

Total Current Assets

19,180

12157

Plant and Equipment

22,000

18,000

(Less: accumulated Depreciation)

Land

9,000

9,000

Total Fixed Assets

31,000

27,000

Total Assets

50,180

39,157

A/c payable

4,500

1,100

Notes Payable

7,200

3,000

Accrued Liabilities

1,300

1,000

Total Current Liabilities

13000

5,100

Bank loan

4,200

4,200

Mortgaged Loan

4,200

5,900

Total Long Term Liabilities

8,400

10,100

Total Liabilities

21,400

15,200

Common Stock (Tk.1Per)

10,000

10,000

Paid In Excess Par

3,000

3,000

Retained Earnings

15,780

10,957

Total Equity

28,780

23,957

Total Liabilities And Equity

50,180

39,157

Answer of Question1:

The No. of Share Outstanding = Book Value per Share × Common stock

= 1 × 10,000

= Tk. 10,000

Sonargao Plumbing

Statement Of Retaining

2010

Beginning R/E

10,957

EAT

10,560

Less: Dividend to P/S

Less: Dividend to C/S

Addition to R/E

Ending R/E

15,780

Hence,

Dividend Paid In 2010 to the C/S = Beginning retaining + EAT (2010) – Retaining Earning (2010)

=10,957 + 10,560-15,780

= Tk. 5,737

In order to answer the Questions 2 & 3 we have calculated the following ratios of Sonargao Plumbing.

Sonargao Plumbing

Ratio Calculation

Ratios

Formula

Calculation(2010)

Calculation(2009)

2010

2009

Industry Average

Liquidity Ratio:

Current Ratio

CA

CL

19180

13000

12157

5100

1.4 Times

2.38 Times

1.4 Times

Acid test (Quick) Ratio

CA- Inv.

CL

19180-11000

13000

12157-6000

5100

0.629 Times

1.207 Times

0.9 Times

Asset Management ratio:

Days Sales Outstanding

A/C receivable

Sales/360

4500

75000/360

2500

70500/360

21.6Days

12.765 Days

45 Days

Inventory turnover

Cost of goods Sold

Inv.

44000

11000

42500

6000

4 Times

7.083Times

5 Times

Total Asset Turnover

Sales

TA

75000

50180

70500

39157

1.494 Times

1.800 Times

1.3 Times

Profitability Ratio:

Gross Profit Margin

Gross Profit

Sales

31000

75000

28000

70500

41.33%

39.71%

30%

Net profit Margin(NPM)

EAT

Sales

10560

75000

11490

70500

14.08%

16.297%

16%

Return On Asset(ROA)

EAT

TA

10560

50180

11490

39157

21.044%

29.34%

25%

Return on Equity(ROE)

EAT

TE

10560

28780

11490

23957

36.69%

47.96%

10%

Debt Management Ratio

Times Interest Earned(TIE)

EBIT

I

15500

840

17000

1050

18.45 Times

16.19Times

12 Times

Market Value Ratio

Earnings per Share

EAT – Div.to Preferred Stock

No. of Share Outstanding

10560-0

10000

11490-0

10000

1.056

1.149

Price Earning Ratio(PE)

Market Price per Share

EPS

22

1.056

18

1.149

20.83

15.665

14

Problems in Sonargao Plumbing Ratios:

Liquidity Position:

1.Weakness in liquidity: The Current ratio for Sonargao Plumbing in 2010 is 1.4 times and in 2009 are 2.38 times. Here the industry average is 1.4 times. Although the liquidity position of Sonargoa Plumbing in 2010 is the same as was in Industry average but with compared to its liquidity position in 2009 is somewhat weak. The weakness in the liquidity can be explained by quick ratio. The quick ratio in 2010 is below the Industry Average and that of in 2009.

2.Holding More Inventories:The reduction of the quick ratio of Sonargao Plumbing in 2010 below Industry average and that of 2009 indicates that it is holding more inventories. If the company can collect the Receivables, it can pay off the Short term liabilities even without liquidating the Inventories.

Therefore our evaluation of the liquidity position of Sonargao Plumbing is fairly poor.

To get why it is in the situation we shall consider the values of Asset Management ratios.

Asset Management:

3.Weakness In Collecting Receivables: The average collection periods of the Receivables for Sonargao plumbing in 2010 is below the Industry Average and more than that of in 2009.With compared to 2009 it is not well enough to collect its Receivables.

4.Low Inventory Turnover: The Inventory turnover in 2010 is below Both Industry Average and that of 2009 which again indicates that Sonargao Plumbing is holding excessive inventories.

5.Low Asset Turnover: The Total Asset Turnover is slightly above the Industry average but it is below the value of 2009 which indicates that its sales have decreased significantly in 2010 with compared the sells performances of 2009.

Therefore after considering the Asset management ratios we have obviously found that Sonargoan Plumbing has a Liquidity Problem and its sales are low.

Profitability of Soanargao Plumbing:

6.Gross Profit: The gross profit margin of Sonargao Plumbing for 2010 is above the Industry Average and that of 2009.

7.Low Net Profit Margin: Although Sonargao Plumbing has good gross profit but its net profit margin (NPM) is below the Industry average and that of 2009 which indicates that its sales are too low and its costs are very high.

8.Low ROA:The ROA for Sonargao Plumbing for 2010 is below Industry Average and that of 2009 which indicates that this low ROA is due to the company’s above average use of debt.

9.High ROE: But the ROE indicates that Sonargao Plumbing has ROE above Industry average and that of 2009. Therefore it has used debt normally not excessively.

Its Debt management is well enough.It will be confirmed after examining the debt Management Ratio.

Debt Management of Sonargao Plumbing:

10.The Times Interest Earned (TIE) of Sonargao Plumbing is above the Industry average and that of its 2009 values. Hence the company is not going to be bankrupt rather it is managing its debt well enough. Its low ROA is due to its low sales and high cost.

Stock Market Performances of Sonargao Plumbing:

11.Price Earning Ratio of Sonargao Plumbing for 2010 is above the Industry Average and that of the values of 2009. Hence It has high Growth prospect.

Strength of Sonargao Plumbing:

Sonargao Plumbing is well enough to manage its Debt.

Sonargao Plumbing is doing well in collecting the Receivables with compared to the Industry Average.

Sonargao Plumbing has a high Growth Prospect in the stock market. It is not a risky firm.

Weakness of Sonargao Plumbing:

Sonargao Plumbing has weak Liquidity.

It has excessive inventories.

It has low sales volume.

It has high cost.

Recommendation: Though Sonargao Plumbing has some problematic areas, it can overcome the problems thus:

By increasing the sales volume giving more emphasize on marketing and sales department performances.

By minimizing the cost to earn the maximum profit.

Keeping the inventory to optimal amount.

Conclusion:In a nutshell we recommend Sonargao Plumbing to be more efficient in managing the asset, maintaining sufficient liquidity, maintaining healthy sales volume and minimizing the cost.